How to read and compare mortgage loan estimates

The Bankrate promise

At Bankrate we strive to help you make smarter financial decisions. While we adhere to strict , this post may contain references to products from our partners. Here's an explanation for .

Key takeaways

- A mortgage loan estimate is a standard three-page document detailing the estimated costs, structure and other terms of the loan.

- Mortgage lenders are required by law to provide borrowers with a loan estimate within three business days of receiving the loan application.

- The loan estimate helps borrowers understand the complete cost of their mortgage and makes it easier for borrowers to compare loan offers.

A mortgage loan estimate spells out the estimated costs associated with obtaining a home loan, whether you’re buying a home or refinancing to a new loan. Here’s our breakdown of what exactly this document entails, what to look for when you review it and how it can help you find the best mortgage for your needs.

Why compare mortgage loan estimates?

What is a mortgage loan estimate?

A mortgage loan estimate is a standardized, three-page document from a lender containing details about a mortgage. While the information in the document is a good faith estimate — in other words, not final — it gives borrowers a comprehensive overview of the costs they’ll likely incur so they can compare offers and prepare and budget appropriately.

“This helps a buyer to understand, at the beginning of the process, the estimated cost of the transaction,” says Stephanie McAllister, a senior mortgage consultant at Prosperity Home Mortgage in Atlanta, Georgia.

When will I get the mortgage loan estimate?

Mortgage lenders are required by law to provide borrowers with a loan estimate within three business days of applying for a mortgage or refinance.

What is included in your mortgage loan estimate?

A mortgage loan estimate includes the following key details:

- Interest rate and annual percentage rate (APR)

- Detailed monthly payment estimate

- Itemized closing costs, including third-party fees

- Prepaid interest

- Escrow expenses

All lenders are required to use the same loan estimate document, a standard that was implemented by the Dodd-Frank Act of 2010.

“Similar to nutrition labels, loan estimates are legally required to look identical across all lenders,” says Emanuel Santa-Donato, senior vice president at Tomo, a Stamford, Connecticut-based mortgage lender. “That way, it’s easy for you to compare loan offers and harder for lenders to hide fees.”

How to read your mortgage loan estimate

You’ll receive a loan estimate whether you’re purchasing a home or refinancing. In either case, use the document as a guide for budgeting and comparing costs between lenders.

Here’s a loan estimate example broken down by page and section. You can view a similar, interactive visual on the Consumer Finance Protection Bureau’s website.

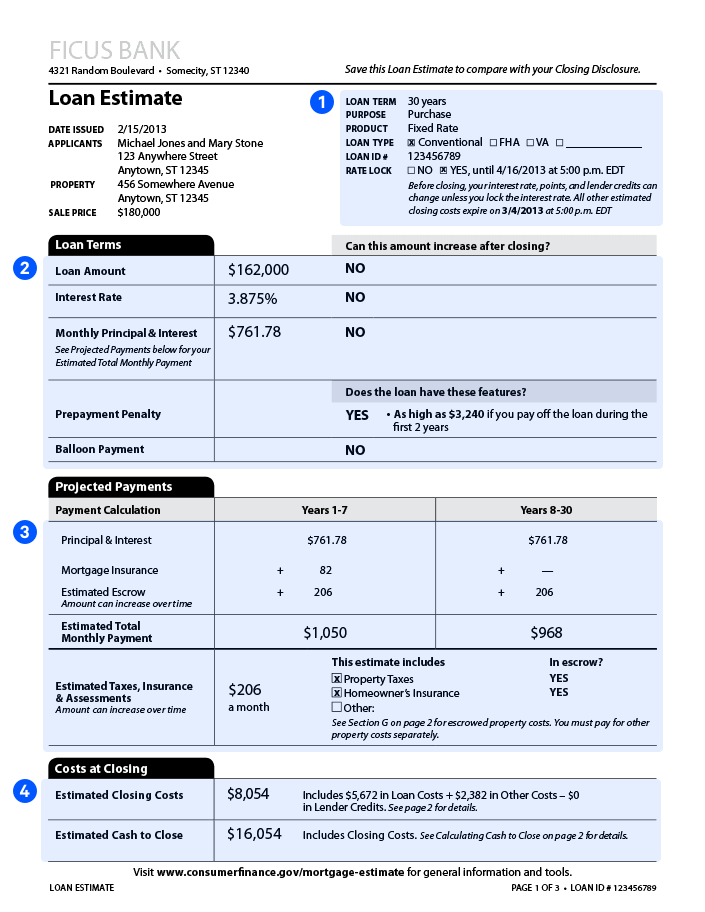

Loan estimate example: Page 1

The first page of the loan estimate outlines three general terms of the mortgage, including:

- Terms of your loan

- Your projected payments

- Closing costs

These details help you understand how much the loan will cost you. For instance, in section No. 1, notice the following information:

- Loan term – The number of years it will take you to pay off the mortgage

- Purpose – If the loan is to purchase or to refinance a home

- Product – Whether the mortgage has a fixed or adjustable interest rate

- Loan type – Whether the mortgage is a conventional loan or some other type, such as an FHA or VA loan

- Rate lock – If the lender has locked the interest rate and when that lock expires

In section No. 2 above, you’ll learn more about the:

- Loan amount – How much you’re borrowing and whether it can be increased or not

- Interest rate – The percentage interest rate you’ll pay, and if it is fixed for the life of the loan or will adjust (and under what terms)

- Monthly principal and interest – The total you can expect to pay for your mortgage payment monthly, not including your homeowners insurance and property taxes

- Prepayment penalty – Stipulates if your lender charges a fee if you choose to pay down the mortgage more quickly or pay it off entirely before the original loan term ends

- Balloon payment – Stipulates if there is a large lump due when the loan term ends

In sections No. 3 and No. 4 above, you’ll find an overview of your payments and costs:

- Payment calculation – This is a breakdown of what you’ll pay monthly, a total that includes principal and interest, any escrow payments or private mortgage insurance (PMI) premiums, if applicable.

- Estimated total monthly payment – This totals up the different components detailed above that go into your estimated regular mortgage payments.

- Estimated taxes, insurance and assessments – You’ll get an estimate of how much your homeowners insurance and property taxes will cost, as well as what funds will be held in escrow.

- Estimated closing costs – This is a total of the various components of your mortgage closing costs.

- Estimated cash to close – This includes closing costs plus any additional money you’ll have to pay upfront, including the down payment, earnest money deposit and any seller concessions if buying a home, along with any lender credits.

Page one also includes the applicant’s name, the date of the loan estimate, the home’s address and the property’s price.

On page one, “you should make sure the interest rate and loan amount listed match what you selected or discussed with the lender,” says Santa-Donato.

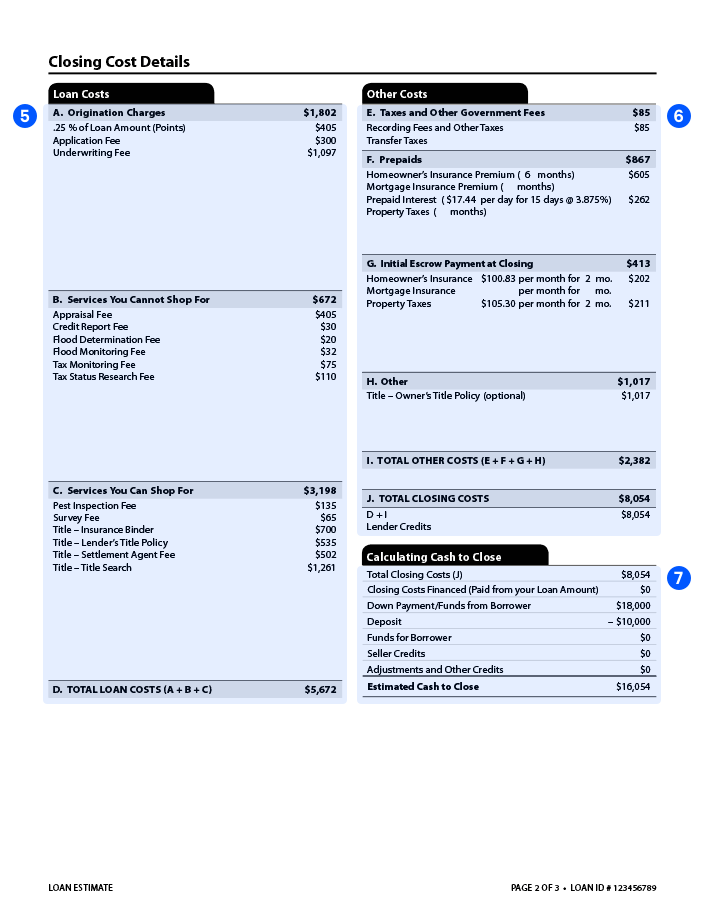

Loan estimate example: Page 2

The second page of your loan estimate, “Closing Cost Details,” also contains three components:

- Loan costs

- Other costs

- Calculating cash to close

This page is where you get a line-by-line breakdown of all your mortgage costs, including fees for required services such as the appraisal and title insurance. The form will delineate which of these you have the option of shopping around for so you can find the best price.

Under “Loan costs,” you get a breakdown of the following services along with their costs in the left-hand column:

- A: Origination charges – Your lender charges a fee for initiating the mortgage, which can include charges for the application and other services, plus any mortgage points you’re buying upfront to lower your interest rate.

- B: Services you cannot shop for – This details the services you’re required to pay for to close the mortgage, such as an appraisal and a credit check, along with what those services cost.

- C: Services you can shop for – This is a list of additional required services, such as a property survey and title search, and how much they cost. The difference between this and the list above is that you have the option of shopping around and comparing providers and costs.

- D: Total loan costs – This is the total sum of parts A, B and C.

Section No. 6 details other miscellaneous costs and charges. These include:

- E: Taxes and other government fees – This part of the estimate includes fees for recording the mortgage with the city or county, as well as property transfer taxes if applicable.

- F: Prepaids – A category that comprises costs like homeowners insurance premiums, mortgage insurance premiums and property taxes.

- G: Initial escrow payment at closing – You have to pay upfront for the items that will go in escrow, including your initial homeowners insurance premiums and your first property tax installment.

- H: Other – This includes any extra additional and sometimes optional costs, such as an owner’s title insurance policy.

- I: Total other costs – The sum of parts E, F, G and H.

- J: Total closing costs – The sum of parts D and I.

The final section on the second page of the loan estimate, “Calculating cash to close,” provides a breakdown of each and every cost you’ll have to pay at the closing, including the down payment and total closing costs calculated in part J of the estimate document. This is the full estimated amount of cash you’re required to have on hand when you close on your mortgage.

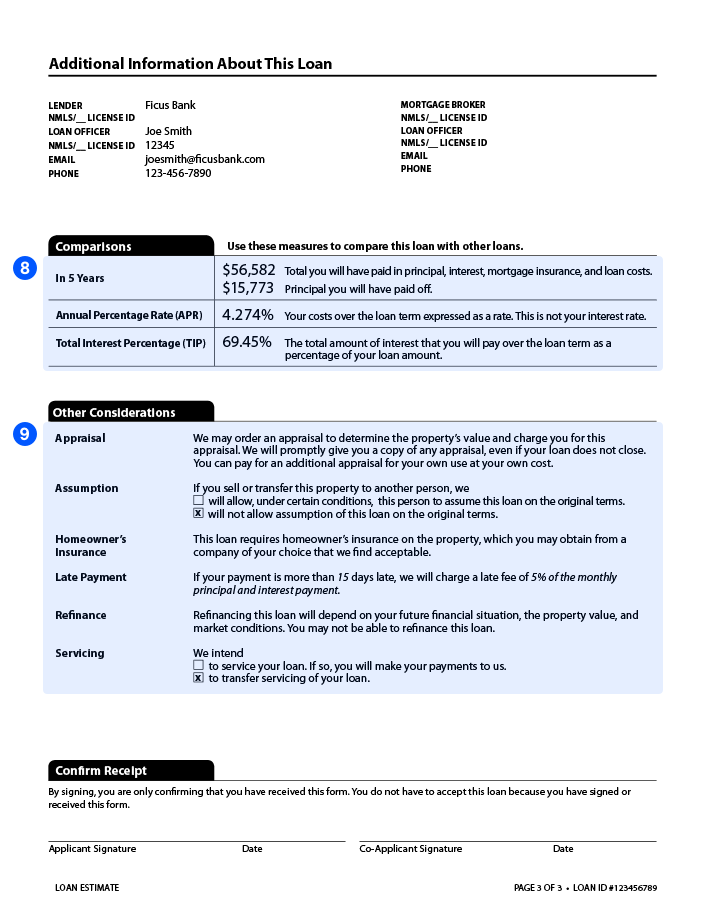

Loan estimate example: Page 3

The final page of the loan estimate lists more important details of your mortgage agreement, like the names of the lender and the loan officer, plus three key figures you can use for comparison shopping in section No. 8 as shown above:

- Amount of the loan principal you will have paid off after the first five years of your mortgage term, as well as the combined principal, interest and (when applicable) mortgage insurance costs

- Annual percentage rate, or APR, which is the combined cost you will pay over the entire loan term, expressed as a rate (not your interest rate)

- Total interest percentage, or TIP, which is the amount of interest you’ll pay over the term of the loan, calculated as a percentage

The final page also explains other parts of the mortgage payment process and your responsibilities as the borrower. This spells out, for instance, your appraisal and homeowners insurance requirements, whether or not the loan can be assumed, any late payment penalties and whether the loan will be serviced by the lender or sold to a separate entity that will service it.

How to compare mortgage loan estimates

When comparing offers between mortgage lenders, follow these tips:

- Pay attention to where the estimates differ on interest rate, origination charges and points.

- Compare the bottom line of the estimated monthly payment and the estimated cash to close.

- Focus on the costs in parts A, B and C, which list origination charges and fees for the services for which you can’t and can shop around. For the services you can get an alternative provider for, keep in mind that your lender might have a partnership with that vendor that includes a preferential rate.

- Note any third-party fees that appear in one lender’s loan estimate and not another’s.

- Look for any lender credits you were promised verbally. If they don’t appear on the loan estimate, ask your loan officer for clarification.

- If you’re refinancing, keep an eye out for any differences in the loan amount between lenders. If you’re obtaining a no-closing cost refinance, make sure you understand how those closing costs are accounted for.

Related Articles

How to calculate your home equity — and how much of it you can tap

How to get the best mortgage rate: A guide to finding the lowest rate